Blogs are opinion pieces and reflect their author’s views

A Top-Up to the Federal Gas Tax Fund for Financing Local Infrastructure

Written by: Almos T. Tassonyi

In stark contrast to the level of respect shown to the third order of government in general and the City of Toronto in particular by the Province of Ontario, the Government of Canada has renewed its commitment to funding local infrastructure.

In response to continuing concerns regarding the local infrastructure deficit in many municipalities and in First Nation communities, the 2019 Federal Budget proposed a one-time transfer of $2.2 billion. The one-time transfer effectively doubles the federal commitment this year to funding incremental municipal infrastructure across the country.[2] Historically, the Federal Gas Tax fund has provided stable federal funding for local infrastructure projects since its inception in 2005. It was made permanent in 2011 at $2 billion per year, and starting in 2014, is indexed at 2% per year applied in $100 million increments. $21.8 billion is committed through the current ten-year agreement (2014-2023).[3]

Allocation of the Gas Tax funds to each province are based on a per-capita entitlement and for 2019-2023 will be based on the 2016 Census data.

Federal Gas Tax funding dollars can be used flexibly to address local priorities. Municipalities can invest funds in the construction, enhancement, or renewal of local infrastructure, improve long-term plans and asset management systems, or bank funds to support future projects. The latter features of the program provide flexibility to local governments to set their own priorities.

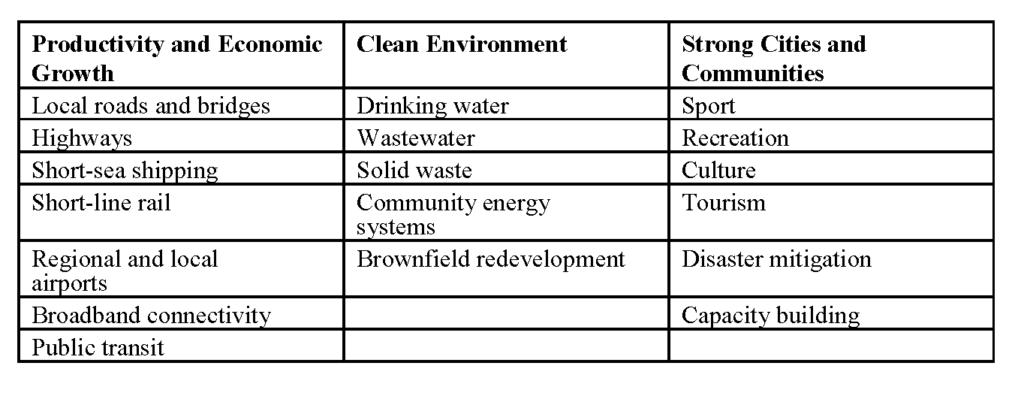

These funds can be invested across 17 project categories grouped under the following broad categories as well as capacity building generally.

Notably, investments in health infrastructure (hospitals, convalescent and senior centres) are not eligible.

The eligibility criteria are set out in the administrative agreements that have been concluded with each Province, and in addition, in British Columbia with the Union of British Columbia Municipalities and in Ontario with the Association of Municipalities of Ontario (AMO) and the City of Toronto. These agreements cover the details of the per capita allocations at the provincial level.[4]

The administrative agreements contain some unique provisions that seek to constrain municipalities on one hand and provide flexibility on the other. These include “incrementality” and banking funds over time. Municipalities have agreed to not replace or displace existing sources of funding for capital investment nor use these funds to reduce municipal taxes. Incrementality is defined with respect to the base amount of municipally funded capital spending that took place in 2000-2004.

Based on the provisions of the administrative agreements and the immediacy of the Federal Gas Tax top up, the choice of investment priorities should be heavily influenced on the results of their respective Asset Management Plans. These plans, as required by the agreements, are used to guide planning and investment decisions in the context of performance measurement methodology consistent with provincially approved guidelines. For example, in Ontario, the information and analysis that must be included is outlined in “Building Together: Guide for Asset Management Plans.” Further, municipalities must continually improve and implement their asset management plans according to the requirements of Asset Management Planning.

Regulations, such as O.Reg. 588/17 in Ontario, which expands on the requirements of municipal Asset Management Plans to identify and plan for exogenous variables (e.g. changes in population and economic growth and vulnerabilities caused by climate change). The current Provincial government in Ontario seems to be completely unaware of this regulation in its current policy decisions that will foist more auditing on municipalities.

Municipalities may also bank their annual allocation for a period up to five years in an approved investment vehicle as set out in the agreements. In Ontario, this includes both investment vehicles approved by statute as well as the investment fund administered by AMO and the Municipal Finance Officers’ Association. Banking provides municipalities with increased flexibility to better accumulate sufficient capital and to plan spending decisions on a more rational and informed basis than a simple “shovels in the ground” approach to spending.

The current agreements have also streamlined the intergovernmental audit of the outcomes of the program. Municipalities must report on the benefits of completed projects, as well as demonstrate adherence to Asset Management Plans and the prioritization of projects. Outcome and output indicators have been put in place at federal and provincial levels.

While the increased funding to municipalities is generally received in a positive manner by municipalities, there is a broad consensus from various perspectives as to the issues of concern in the rationale, design, application, administration, and outcomes of intergovernmental transfer arrangements.[5]

Generally, federal funding of local infrastructure is rationalized as a way to overcome fiscal externalities, whether vertical or horizontal, to solve the issues of fiscal imbalances related to differences in the marginal costs of raising taxes. Federal funding programs for local infrastructure can also receive positive political support in the pursuit of national objectives including the promotion of equal opportunity in all regions or to ensure that standard minimum levels of service are met at a local level. However, there can be significant difficulties in measuring externalities and imbalances in the marginal cost of public funds, which can lead to ambiguity on the effectiveness of the transfer program in addressing perceived externalities.[6] Appropriate levels of service standards are more commonly defined, and more easily measured, by engineering or science-based quality standards such as those used to define potable water

quality or levels of contaminants left in effluent. Technical and health standards are more feasibly nationally or provincially mandated, making outcomes from federal transfers easier to identify and promote.

Conditional grants can have a “corrosive” effect on local accountability and fiscal management. The most common criticisms include the creation of incentives for distortions resulting from local mispricing of service provision and avoidance of hard decisions on the appropriate levels of taxes and fees;, biasing the prioritization of local expenditures in order to receive matching funding thus negatively affecting long-term fiscal and capital investment planning; and depending on the allocation methodology, ignoring the fiscal capacity and needs of the municipal jurisdictions.[7]

It should be noted that the design of the Gas Tax Fund represents a serious effort to deal with the critiques of conditional transfers from the federal government. In particular, the program has avoided ad-hoc based transfers through a long-term funding base and long-term agreements on the allocation of the fund. While the per capita basis of the allocation does not address fiscal needs or capacity concerns directly, this method has general acceptance due to equity and transparency in its administration. Further, the existing contractual framework does attempt to address fungibility through the measurement and auditing of incrementality. Admittedly, the current top-up may be perceived as a policy decision in direct contrast to recent initiatives in various provinces in the context of provincial-municipal fiscal relations. However, this program respects local governments as the “third order” of government and provides a significant degree of flexibility in its permissive framework.

[1] A previous version of this blog was published in the May 2019 issue of the Public Sector Digest. Helpful comments from Chris Van Dooren of AMO and William Kluska are gratefully acknowledged.

[2] (Canada, 2019)

[3] These comments are based on reports and agreements found at https://www.amo.on.ca/AMO-Content/Gas-Tax/Canada-s-Gas-Tax-Fund

[4] (Dupuis, 2016)

[5] For example see (Bazel & Mintz, 2015), (Slack & Tassonyi, 2016), (Boadway & Kitchen, 2018) and most recently Bird (2018).

[6] (Dahlby & Jackson, 2015) explore this concept of the marginal cost of public funds and its implications for grant design.

[7] See (Cote & Fenn, 2014), (Tassonyi & Conger, 2015) , (Slack & Bird, 2018) and (Kitchen, 2019)

Association of Municipalities of Ontario. (2014). Guide to the Municipal Funding Agreement for the Transfer of Federal Gas Tax Funds April 2014. Toronto. Retrieved April 30, 2019, from https://www.amo.on.ca/AMO-Content/Gas-Tax/Canada-s-Gas-Tax-Fund

Bazel, P., & Mintz, J. M. (2015). Optimal Public Infrastructure: Some Guideposts to Ensure We Don’t overspend. SPP Research Papers, University of Calgary, School of Public Policy. Retrieved from https://www.policyschool.ca/wp-content/uploads/2016/03/optimal-public-infrastructure-bazel-mintz.pdf

Bird, R. M. (2018). Policy Forum:Equalization and Canada’s Fiscal Constitution-The Tie That Binds? Canadian Tax Journal/Revue Fiscale Canadienne, 66(4), 847-69.

Boadway, R., & Kitchen, H. (2018). A Fiscal Federalism Framework for Financing Infrastructure. In J. R. Allan, D. L. Gordon, K. Hanniman, A. Juneau, & R. A. Young, Canada: The State of the Federation 2015 Canadian Federalism and Infrastructure (pp. 75-113). Montreal and Kingston: McGill-Queen’s University Press.

Canada, G. o. (2019). Budget 2019. Finance. Government of Canada. Retrieved April 30, 2019, from https://www.budget.gc.ca/2019/home-accueil-en.html

Cote, A., & Fenn, M. (2014). Provincial-Municipal Relations in Ontario:Approaching an Inflection Point. IMFG Research Paper, Munk School of Global Affairs and Public Policy, University of Toronto, Institute on Municipal Finance and Governance, Toronto. Retrieved from https://tspace.library.utoronto.ca/bitstream/1807/81250/1/imfg_paper_17_cote_fenn_May_22_2014.pdf

Dahlby, B., & Jackson, E. (2015). Striking the Right Balance:Federal Infrastructure Programs, 2002-2015. SPP Research Paper, University of Calgary, School of Public Policy. Retrieved from https://www.policyschool.ca/wp-content/uploads/2016/03/federal-infrastructure-transfer-dahlby-jackson.pdf

Dupuis, J. (2016). The Gas Tax Fund: Chronology, Funding and Agreements. Library of Parliament, Economics, Resources and International Affairs Division,Parliamentary Information and Research Service. Retrieved April 30, 2019, from https://lop.parl.ca/staticfiles/PublicWebsite/Home/ResearchPublications/InBriefs/PDF/2016-99-e.pdf

Kitchen, H. (2019). Beyond the Property Tax: What Taxes for Large Cities? In E. Slack , L. Philipps, L. M. Tedds, & H. L. Evans, Funding the Canadian City (pp. 75-95). Toronto: Canadian Tax Foundation.

Slack, E., & Bird, R. M. (2018). Financing Regional Public Transit in Ontario: The Case for Strengthening the Wicksellian Connection. In J. R. Allan, D. L. Gordon, K. Hanniman, A. Juneau, & R. A. Young, Canada: The State of the Federation 2015 Canadian Federalism and Infrastructure (pp. 45-74). Montreal and Kingston: McGill-Queen’s University Press.

Slack, E., & Tassonyi, A. (2016). Financing Urban Infrastructure in Canada: Overview, Trends and Issues. Toronto: Institute on Municipal Finance and Governance, Munk School of Global Affairs, University of Toronto.

Tassonyi, A. T., & Conger, B. W. (2015). An Exploration into the Municipal Capacity to Finance Capital Infrastructure. SPP Research Paper, University of Calgary, School of Public Policy. Retrieved from https://www.policyschool.ca/wp-content/uploads/2016/03/municipal-capital-infrastructure-tassonyi-conger.pdf

by Almos T. Tassonyi

Dr. Almos Tassonyi is an Executive Fellow and former Director of the Urban Policy Program at The School of Public Policy, University of Calgary. He is an Adjunct Lecturer, Department of Geography and Planning, University of Toronto, and a Research Associate at the International Property Tax Institute.

He has over thirty years of experience working in the Ontario Ministries of Municipal Affairs and Finance on municipal fiscal issues and international experience in China, Hungary and India working with the World Bank, the Forum of Federations and the Canadian Urban Institute.

Dr. Tassonyi holds a PhD in economics from the University of Calgary, an MSc in Economic History from the London School of Economics and a bachelor’s and master’s degree in Economics and Economic History from the University of Toronto.